OPINION: IN Australia we are continuing to come to grips with the evolving state of play around the future effects of COVID-19 on society and within virtually all parts of the economy.

There now seems to be somewhat of a stabilisation around the containment of the Virus which has seen some welcome easing of social distancing restrictions in some states. These signs of positivity over the past week are only small yet, relatively speaking, significant steps forward as all Australians look forward to a return to a restriction free and `normal’ lifestyle.

One of the potential dangers that has emerged over the past couple of weeks is the tendency to allow negativity to seep into our thinking about the path forward for the property industry.

I know from a personal point of view that given my natural DNA as an optimist, as soon as the trend started to shift away from only negative stories on the news to some stories that were of a positive nature I started to feel that maybe this isn’t going to be so bad after all.

While that feeling may end up being correct it remains too early and the issues still too complex to be able to make any predictions of what is to come for our industry.

Whilst there have been numerous temptations to make bold predictions, as a collective group of professionals within our team at CBRE we have opted to focus on what we can control on a day to day basis and to then share with the marketplace the most pertinent themes.

CBRE Melbourne Commercial Sales Transaction Update:

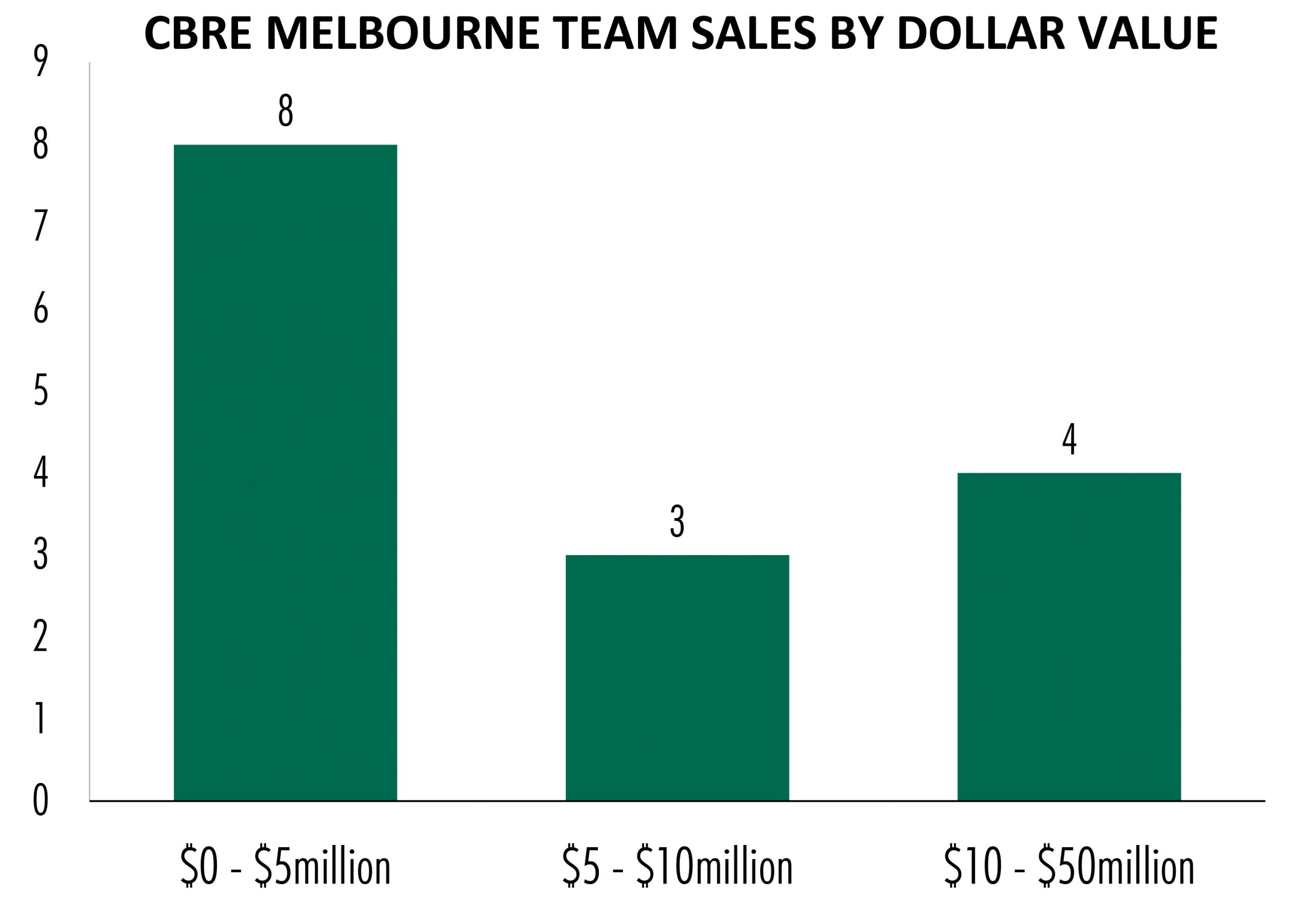

The level of transactional activity completed by our team since March 11th 2020 (Covid-19 declared a pandemic) has been pleasing. A total of nine properties have been sold during the period March 11th 2020 – May 2nd – 2020 with total sales totalling just under $130 million.

We have seen early during the COVID period the sale of a shopping centre for above $30 million, and as recently as last week saw the largest dollar transaction take place with the sale of 355 Spencer Street in West Melbourne for $38.5 million. We are also noticing somewhat of a return of confidence stemming into sales activity within our strip retail investments business with 3 properties in this sector all price under $5 million selling last week.

Emerging Trend #1 – Highly credentialed and experienced property players are continuing to make new acquisitions

Over the past four weeks, we have seen several transactions announced across various sectors within the Victorian commercial property market. These transactions have ranged from deals in the development site space, to the strip retail space and within the commercial office building space.

In looking at these transactions a little closer, one consistent theme has been that many of the buyers have been well known, well regarded and highly sophisticated players.

Again it is too early to be making bold predictions about what the future in 6 to 24 months may look like, but the confidence and subsequent action being taken by these experienced players can certainly be seen as a positive.

Below is a list of buyers across the wider industry (not just CBRE transactions) who have completed transactions in the past 30 or so days.

- Prime Value – Yak Yong Quek

- Blue Earth Group – Michael & Omran Dib*

- Golden Age Group – Jeff Xu*

- Trenerry Property Group – Robert DiCintio

- Avari Funds Management – Alan Liao*

- Chemist Warehouse – Sam Gance*

*Sales transacted by CBRE Melbourne Commercial Sales Team

It would be fair to say that the transactions took longer than usual to complete and in some instances were not unlike the experiences that I had in completing deals post the GFC (2008-2010).

We will continue to keep an eye on the buyers that are behind future successful transactions and keep you updated and look forward to observing if there continues to be a consistent level of activity from buyers of this nature.

It would be fair to conclude that if experienced buyers remain active that they are seeing some elements of positivity ahead for both the residential and commercial property industry.

One of the potential drivers for these types of groups may well be their strong standing with their banks and or financiers. These relationships may be providing a heightened level of confidence both on the availability of debt for commercial property acquisitions, as well as the pricing of that debt today and over the next couple of years.

Emerging Trend #2 – Mainland Chinese Enquiry and Activity

Another emerging trend has been the increase in enquiry that our team is currently seeing come directly out of mainland China.

Through our Asian Capital Services team, headed by Lewis Tong whom I’ve worked directly with for over a decade, we are in a very good position to pick up on early changes with enquiry patterns coming directly out of Asia.

The past

During the years 2009 to 2017 it is fair to say that the impact of Chinese investment both in the Australian residential and commercial property markets had to be seen to be believed.

Chinese purchasers made plays in all sectors across the various markets from the more traditional asset classes – commercial office buildings, hotels, shopping centres – to the less traditional including wineries, golf courses and function centres.

It could be argued that over this period they were most active in the development site space with a diverse range of both smaller, medium and large developers acquiring sites and, contrary to many of the pessimistic views at the time, getting on with delivering projects on those sites and often then moving onto the next project.

The sheer significance of the capital which they invested in both the residential and commercial sectors had a major influence on both federal and state government property taxation policies as well as policy that would be created by the big four Australian banks.

Chinese capital became one of the major drivers in the Australian property and building industries recovering from the damage caused during the GFC with a significant flow-on effect for businesses across the industry including architects, town planners, agents, lawyers, and builders.

Whilst many felt that the major reduction in Chinese buyer transactions over the past 18 months had been due to changes to property taxes and the big four banks policies towards foreign investment, this was not the case.

In late 2018 the Chinese government introduced sweeping and extremely serious policy relating specifically to clamping down on funds exiting China for investment into commercial property in other countries.

One theme that has been consistent across the many years that both Lewis and I have been dealing with both private and institutional property buyers based in China is that they have a very strong adherence virtually on an immediate basis to any instruction that is provided by their government and outflow capital controls was met with the same level of adherence.

The new policy virtually brought an instant halt to Chinese buyers investing in the Australian market resulting in a very low level of transaction volumes during this period. There has been the odd transaction completed with Chinese buyers since Q4 2018 but most of these buyers were early movers into the Australian market who had either made significant profits from successfully completed developments or were able to access large amounts of capital that had already been sent from China.

During the GFC many local players, both investors and developers, sat on the sidelines and the reasons were twofold. The first was the prediction that values would continue to fall and that it would be prudent to wait for this to occur before stepping in. The second was that buyers who wanted to acquire assets found it difficult to both find debt and further obtain an acceptable return based on the price of the debt.

The present

While it might be a little early to say Chinese investors are back there is no doubt that the recent increase in enquiry coming out of China, which really only started as the COVID-19 issue gained momentum, has been significant.

The enquiry has come from private investors and private families as well as from some of the larger property companies that operate within the Chinese market. In addition we have also seen a pick up in engagement from intermediary firms that are related to the property industry such as accountants, lawyers and private bankers.

The reasons are as yet unclear and may include the fall in value of the Australian dollar along with the historical and familial ties that Chinese investors have with Australia and Melbourne in particular, but we also wonder if this surge in enquiry could be a signal that the capital controls, at some point in the near future, may be eased and reopen the door for Chinese buyers.

If Chinese capital was again unleashed on the Australian property sector I have no doubt it could very well have a similar impact on the market as it had prior to the introduction of the capital control laws.

I also have no doubt that Chinese capital would be very much welcomed by the industry with many participants having enjoyed positive dealings with Chinese capital during the years of 2009 to 2017.

Emerging Trend #3 – Increased activity from sub $5 million investors

Over the past 10-14 days, our team has observed a significant increase in enquiry for properties with a value of $5 million or less. These properties are commonly freehold retail assets located in Melbourne’s well known shopping strips as well as smaller commercial office assets located on the Melbourne CBD fringe and across several suburbs within a 10km radius of the CBD.

We are unsure what the drivers of the increased interest are however we can confirm that the interest is also flowing into new transactions being successfully completed with multiple parties.

As mentioned previously in this update, it wouldn’t be a surprise to us if the access to debt and the pricing of that debt was playing a significant role. Also apparently significant here is the lack of suitable returns coming from other investment options.

It has been clear to see that even the biggest of stock market investors are feeling the effects of what has been a very volatile period for the ASX and no doubt this would flow down to smaller players that are considering investing into the stock market.

The recent surge in deal activity handled by our strip retail investments team has also thrown up an interesting opportunity for reflection and analysis.

At a time when smaller retailers are doing it harder than ever, what are these buyers seeing that is giving them the confidence to pursue and complete new purchasers?

There have been a couple of trains of thought. One theme is that many retailers through this COVID-19 period have been forced to bring forward any plans they may have been sitting on to provide a digital platform to their customers in addition to their bricks and mortar offering. We have seen a wide range of businesses quickly pivot to adding an online offering to ensure that their business has stayed relevant and active with existing customers.

We see this only as a positive that can come out of COVID-19 for landlords with their tenants set to benefit from having a dual platform to generate sales which ultimately improves their viability.

The second train of thought relates to the movement of customers. Is it likely that consumers will want to stay away from large shopping centres in the wake of what they have experienced through the COVID-19 period?

If this is the case we believe that strips around Melbourne that will benefit most in the near term are those that are located within precincts that provide customers with a high level of accessible and convenient car parking.

We look forward to being in a position in the coming weeks to provide you with further updates in relation to this part of the market with a host of properties being handled at present by our team in both the early and late stages of negotiation.

Conclusion

Whilst there remains a very high degree of uncertainty within both the residential and commercial property markets it has been pleasing to see a respectable volume of transactions being completed in the marketplace.

We are experiencing a very low volume of new listings at present as vendors continue to observe both the progress of the virus as well as putting their thoughts into what the likely, short, medium and long term impacts might be.

These questions are all very valid but equally very difficult to answer due to the virtual daily changes that are occurring as governments and various health departments evolve their strategies to combat and defeat the virus.

Without doubt there has been an improvement in sentiment within the property industry over the past couple of weeks however it would not be surprising in the coming weeks to see this shift again due to the sheer abnormality of the conditions that both the society at large and the economy is currently facing.

Our team at CBRE will continue to engage with the widest possible pool of potential buyers based locally, interstate and overseas in order to deliver the best results for our clients, an approach which to date has yielded a range of really pleasing results.

I look forward to providing you with further thoughts and analysis as more experiences and information come to hand.

By Mark Wizel, National Director, CBRE Australia.

Mark Wizel is Director Investments with CBRE and heads up a 64 strong team in the sub $100 million market sector with more than $14 billion in sales since 2009.

Mark is highly regarded for his knowledge of capital flows from Asia and has been prominent in sales of retail centres and development sites across Melbourne. He has been a regular commentator and speaker on commercial property over the last 10 years with a focus on Asian, and particularly Chinese, investment.